Your company has chosen to informally fund its nonqualified deferred compensation plan (NQDCP) with Corporate-Owned Life Insurance (COLI). Like many plan sponsors, you have determined that COLI is a tax-efficient way to finance and recover the costs of your NQDCP. This guide will help you move from your prepurchase due diligence process to implementation and management of your COLI. We will start with an outline of the regulations governing COLI, move to a discussion of the implementation process, review COLI accounting, and finish with an overview of how to best manage your COLI on an ongoing basis.

COLI Regulations

Internal Revenue Code (IRC) §7702: This code section defines the rules by which COLI cash values can grow on a tax-deferred basis. Additional guidance on this subject is included in IRC §72. IRC §7702 also outlines the rules by which a company can receive COLI insurance proceeds on a tax-free basis.

IRC §7702A and IRC §7702(f)(7): These code sections outline the rules by which COLI cash values can be accessed on a tax-free basis via withdrawals to basis and loans. Additional guidance on this topic is included in IRC §72.

IRC §101(j): This code section outlines implementation steps and ongoing reporting that must be followed in order for the company to receive COLI insurance proceeds on a tax-free basis.

IRC §817(h): This code section defines how variable life insurance policies must be structured in order to allow for tax-free reallocations between subaccounts.

The COLI Implementation Process

The steps to implementing a COLI program are fairly straightforward. However, they are different in some ways from qualified retirement plans such as 401(k) program, since they include documentation specific to life insurance.

Key issues addressed during the implementation processes:

How is a COLI Purchase Structured? The company is the applicant, owner, and beneficiary of each COLI policy. Only key employees of the company are insured.

IRC §101(j) – COLI Best Practices of the Pension Protection Act of 2006: These rules must be followed to ensure that the company can receive insurance proceeds on a tax-free basis. The insured group must be limited to the top 35% of employees by compensation. The company must obtain written consent of all insured individuals and must also disclose the maximum amount of coverage that may be placed on each individual. Policy amounts are sized to comply with state insurable interest statutes. The company must annually file Form 8925, which contains high-level information about any COLI that is subject to IRC §101(j).

Guaranteed Issue Underwriting: Most COLI is implemented without the need for medical underwriting. Each insured person signs a “Consent to Insurance” form, but no medical exam is required. They are asked to confirm that they are actively at work, typically defined as not being absent from work for more than three to four consecutive days in the past 90 days. They are also asked if they have used tobacco during the last 12 months. The amount of coverage on each person is determined once members of the group who have consented to be insured have been finalized.

Rabbi Trust: A company can choose to hold COLI directly on its balance sheet. However, many companies use a “rabbi trust” to hold COLI instead. Doing so protects assets used to informally fund participant benefits in the event of a change in control or a change of heart by management. The company cannot generally access plan assets for its own purposes; they must be used to pay plan benefits. However, the company can access a portion of the assets if they grow above a set percentage, typically 105% to 120% of plan liabilities. For example, if the threshold is 120% and plan assets grow to 140% of liabilities, the company can access the 20% above the threshold, but the remaining assets must remain in the trust to pay benefits.

Accounting for COLI

ASC 325-30-35 (TB 85-4 and EITF 06-5), entitled “Investments in Insurance Contracts,” governs the accounting for COLI. COLI is booked as an asset equal to its cash surrender value on the balance sheet, and changes in value are recognized as expenses or income on the income statement.

COLI grows on a tax-deferred basis. However, COLI gains and losses are treated as permanent differences under the provisions of ASC 740 (ASC 740-10-25-30) if the COLI is never surrendered or allowed to lapse. If held in this manner, COLI values are not simply deferred from taxation, they are never subject to income taxation. Therefore, there is no tax reporting required on a company’s financial statements for COLI gains and losses.

COLI cash surrender value is booked under other assets, and realized and unrealized investment gains are booked as other income. When a death benefit is paid to the company, the total amount is booked as cash, and the amount that was previously booked as cash surrender value is recorded as a decrease in cash surrender value. The net amount by which the death benefit exceeds the cash surrender value is recorded as other income.

The Interaction Between an NQDCP and COLI

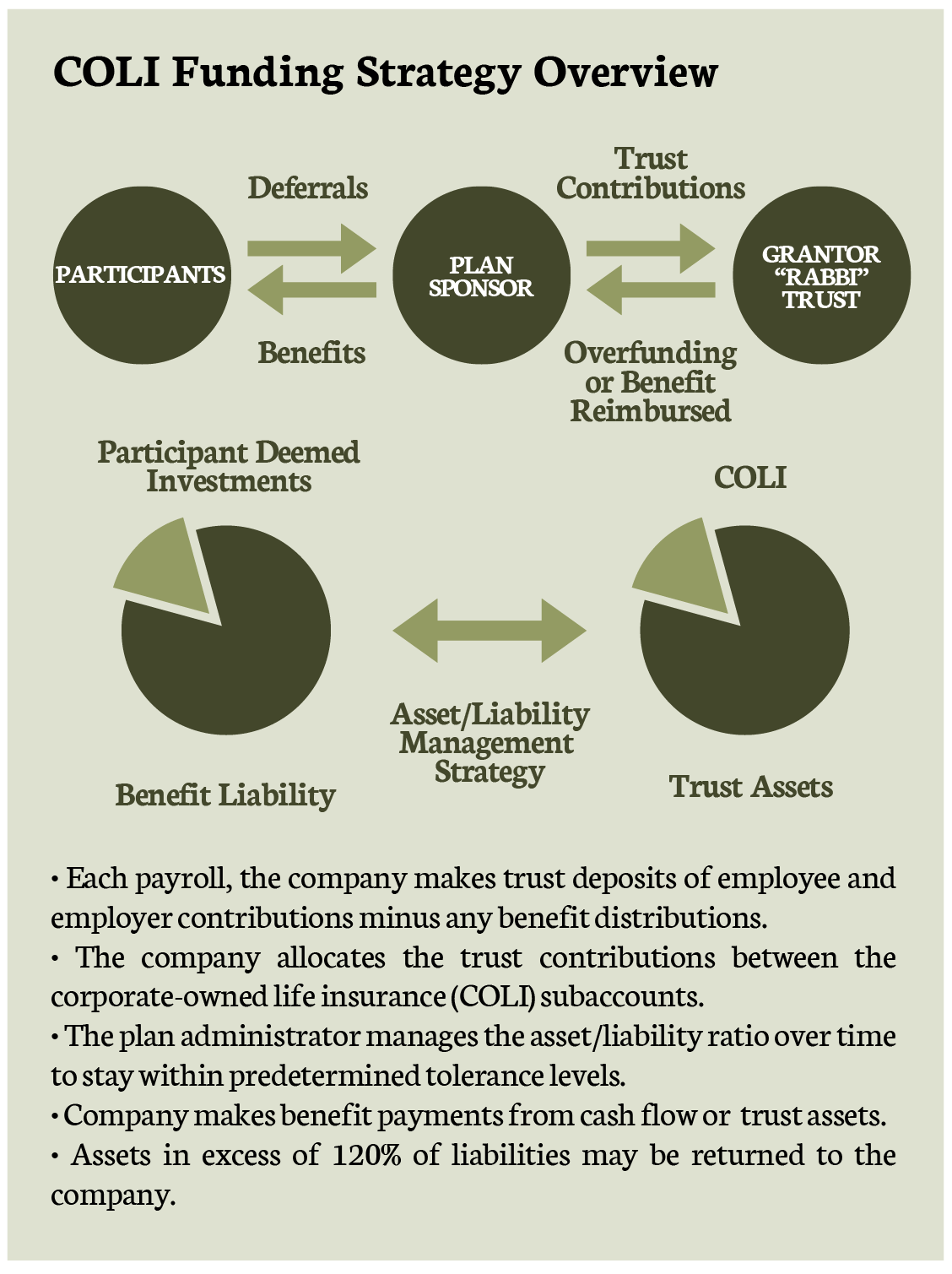

NQDCP employee and employer contributions provide the funding for COLI premiums. In the future, the company may use the COLI cash surrender value to pay plan benefits, or it may pay them from cash flow. Shown at right is a chart summarizing how the NQDCP and COLI interact with each other over time, assuming that a rabbi trust is used to hold the COLI.

Ongoing COLI Management Process

Vendor Selection and Plan Reporting: We will partner with you to select a third-party administrator (TPA) that will help you manage both your COLI and the NQDCP it is informally funding. The TPA will typically provide information about the COLI on a monthly or quarterly basis. TPA reporting will include a record of any premium payments and policy distributions, documentation of movements between subaccount options, and policy death benefits. These reports are often offered on the TPA’s sponsor website, along with additional ad hoc report options. The company uses the information in these reports for ongoing financial reporting and overall plan management.

Asset/Liability Management: One aspect of COLI funding of NQDCPs that is different from 401(k) plans is the relationship between assets and liabilities. In a 401(k) plan, assets and liabilities are almost always identical to each other. Since there is no regulatory requirement to fund NQDCPs at all, assets and liabilities often do not match each other.

For example, a company may offer the existing 401(k) plan lineup as fund options for participants. However, identical funds often don’t exist inside the COLI product, so the 401(k) plan funds are mapped to COLI subaccounts with similar characteristics. Even if the funds offered to participants are identical to the subaccounts inside the COLI, there will always be a difference between the asset and liability values due to the insurance costs of the COLI.

COLI Rebalancing: Companies typically want the fund allocations within assets and liabilities to closely match each other. In some cases, this goal can be achieved by automatically rebalancing assets as frequently as on a daily basis to ensure that the percentage of liabilities held in each participant fund matches the percentage of cash value in the mapped COLI subaccounts. In other cases, companies choose to rebalance only when the difference between funds or classes of funds exceeds a certain tolerance level. For example, rebalancing may occur if the variance is greater than 5% for a given fund, or 2.5% for a given asset class such as equity or income.

Selecting a Benefit Payment Method: While COLI cash value is always an option to pay NQDCP benefits, companies typically choose whether to pay benefits from the COLI or other sources based on their specific financial circumstances. The most common approach in the early years of a COLI plan is to net any distributions that need to be paid from ongoing employer and employee contributions. It is likely that at some point distributions will exceed contributions. When that occurs, the company can decide whether to pay the remaining distribution amount from the COLI, from its general cash flow or from other funding sources, such as lines of credit. A detailed discussion of the factors that determine the proper funding choice is beyond the scope of this report, but we can help you decide which option is best whenever a distribution must be paid to a participant.

COLI Death Benefit Administration: Under federal tax law and state insurable interest regulations, companies are allowed to hold COLI even after an insured person terminates employment. Doing so maximizes the tax benefits of COLI, since all COLI values are tax-free if held until the company receives insurance proceeds upon the death of the insured person. However, that event often occurs many years after the insured person’s termination of employment. The TPA will help track these former employees through tools such as Social Security number sweeps. When a death occurs, the TPA will assist in the collection of the death certificate and processing of the death claim.

Conclusion

While some of the steps required to effectively manage a COLI program are quite different from core benefit arrangements, Wrightwood and your selected TPA can help ensure that this process goes as smoothly as possible. Wrightwood will help you monitor the activities and reporting from the insurance carrier and TPA, help you address any COLI or benefit-related issues that may arise over time, and provide updates on regulatory, legal, or accounting changes that could impact your plan. Please contact Wrightwood if you have further questions.