Tools to address qualified retirement plan refunds.

The Problem

401(k) plans provide valuable retirement benefits for most employees. However, highly-compensated employees (HCEs) can be held back by these plans, since IRS contribution limits are often quite low compared to their incomes. In many cases, HCEs can’t even contribute the full amount normally allowed because a plan has failed nondiscrimination testing. In these cases, contribution amounts are limited or a portion is refunded.

What are Potential Solutions?

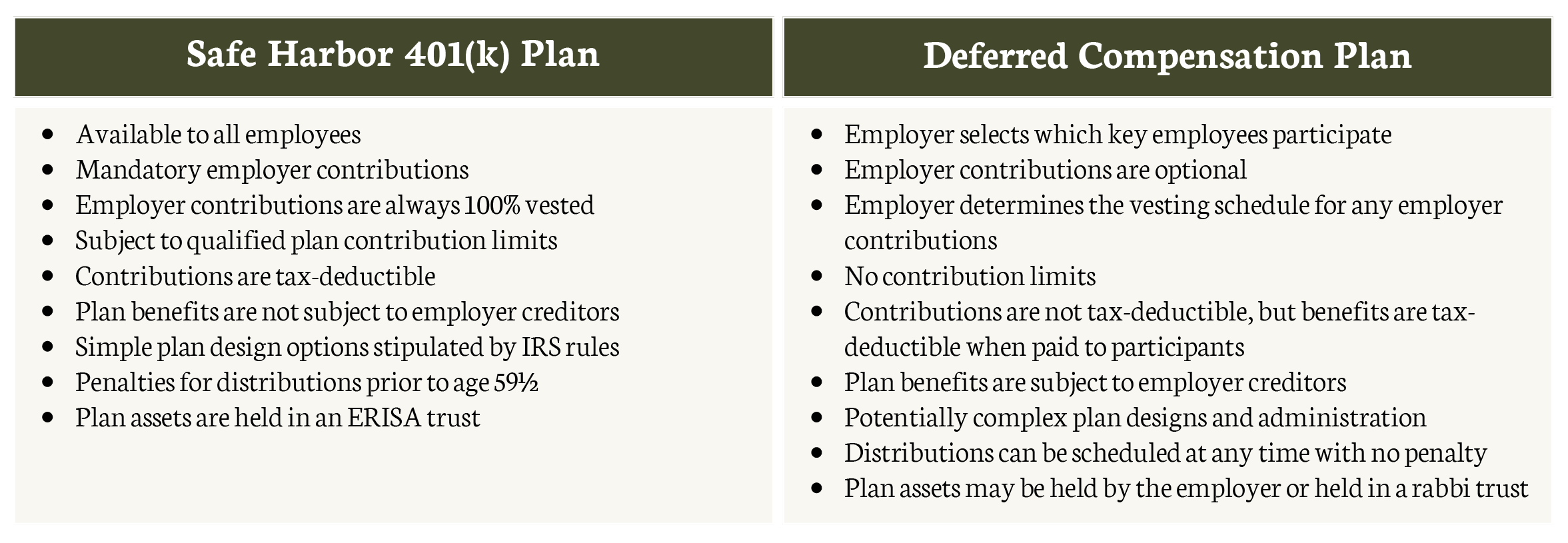

There are two primary tools to address qualified plan refunds; safe harbor 401(k) plan designs and deferred compensation plans (DCPs). DCPs are technically nonqualified, meaning they aren’t subject to restrictive ERISA rules. They often have names like 401(k) mirror plan, excess plan, or supplemental executive retirement plan (SERP). What they all share is a great deal of plan design flexibility and the ability to limit plan participation to a select group of key employees. However, the benefits and risks of DCPs are quite different from safe harbor plans for both employers and plan participants.

The Retirement Plan Design Consulting Process

Plan design flexibility is a key reason employers consider DCPs as alternatives to safe harbor plans. For example, HCEs can defer as much money as the employer will allow. Employers also have complete discretion over the participant group, as well as the size, form, and vesting schedules of employer contributions. Safe harbor 401(k) plans offer a straightforward way to eliminate qualified plan refunds for HCEs, but this design alternative may come at a substantially greater cost than the current design. DCPs offer flexible plan design features that can be customized to match an organization’s recruiting and retention strategies. There is no one solution that will fit all situations, since employers must determine which plan design options best fit their unique financial situations and overall compensation and benefits planning objectives.