Using Non-qualified Deferred Compensation Plan “True-Up”

Features To Restore 401(k) Plan Matching Contributions

Non-qualified deferred compensation plans (NQDCPs) are valuable tools to help highly compensated employees (HCEs) create supplemental retirement income. Participants can defer virtually unlimited amounts of income from taxation, and employers can make optional contributions to these plans as recruiting and retention tools. However, participant contributions to NQDCPs can lead to reduced 401(k) matching contributions if a plan doesn’t include features to help avoid this problem.

The Challenge

While employers have flexibility in how they define compensation in qualified plans such as 401(k) plans, using a definition other than the ones provided in Code Section 415 or Code Section 414(s) safe harbor rules can be time-consuming and costly. Sponsors using alternative compensation definitions must submit detailed information to the IRS that demonstrates these plans don’t favor HCEs, and that they also use compensation definitions that are reasonable and nondiscriminatory. These plans may also be subject to higher IRS fees than plans using prototype documents.

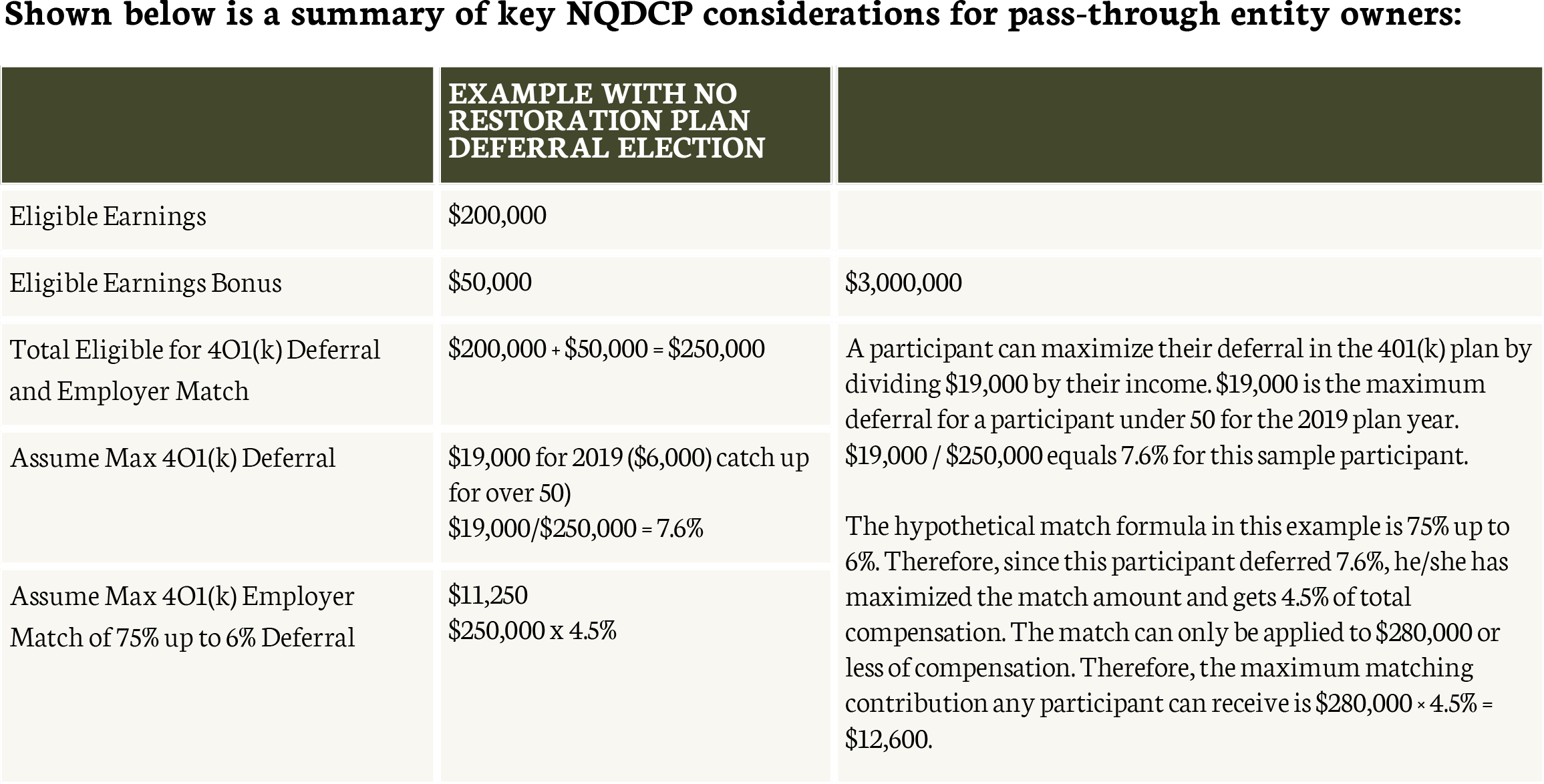

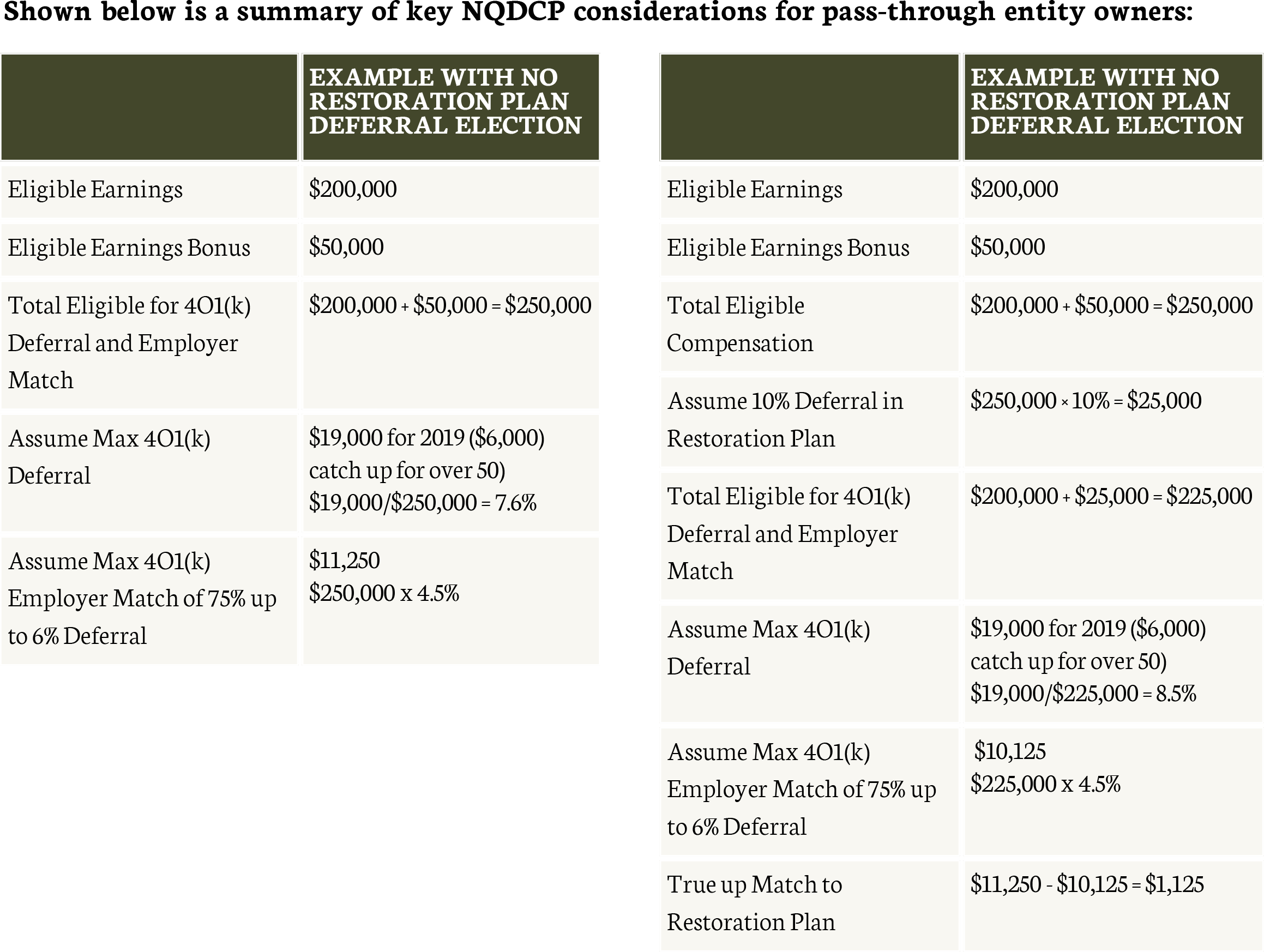

For these reasons, many employers use the Section 415 or 414(s) compensation definitions in their qualified plans. However, both definitions exclude non-qualified plan deferrals from compensation. Therefore, qualified plan matching contributions are only applied to this reduced compensation amount (excluding NQDCP contributions), up to the Section 401(a)(17) income limit ($280,000 in 2019).

The Solution

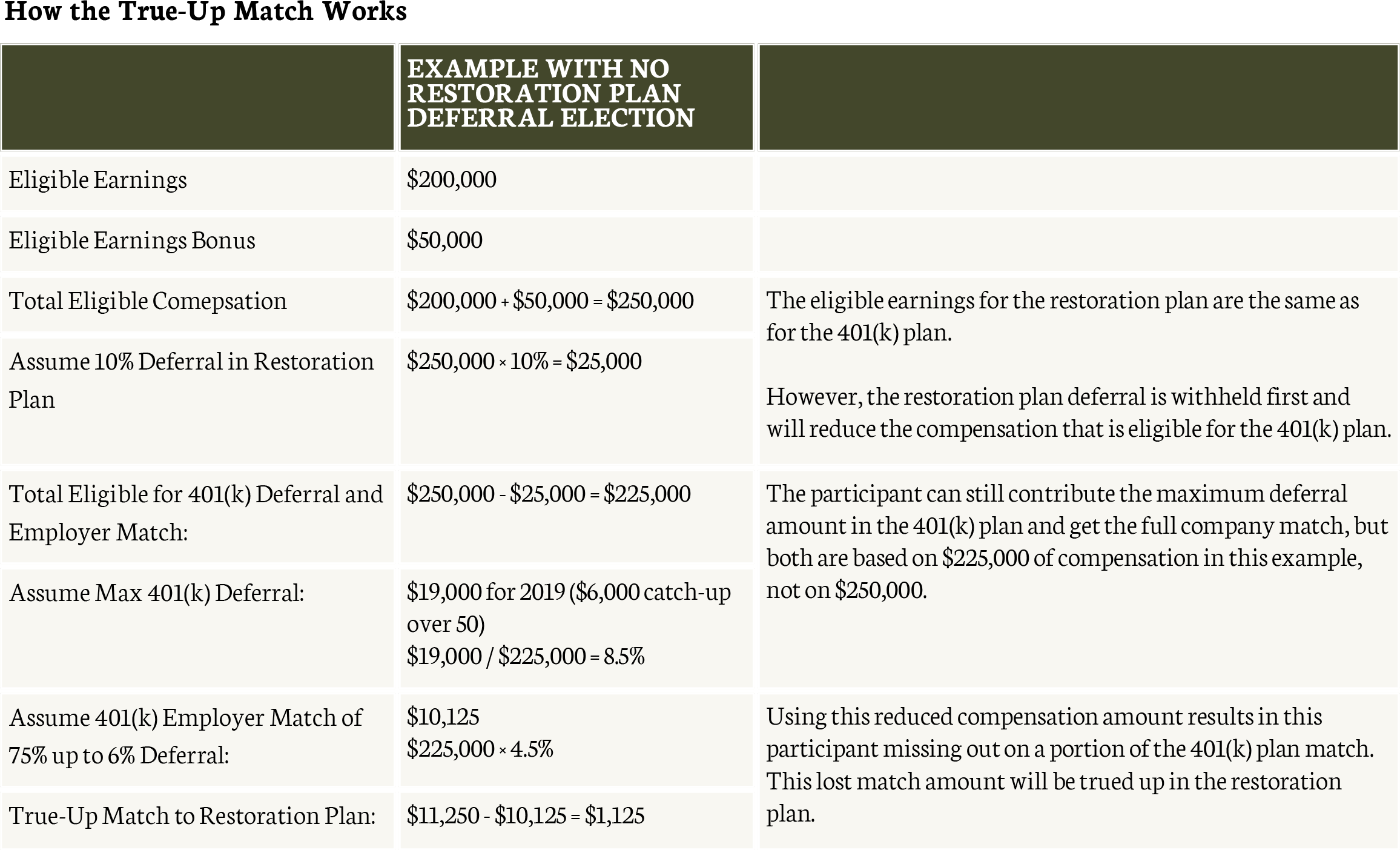

Employers can use “true-up” features in an NQDCP to restore these lost qualified plan employer contributions. In its simplest form, a true-up feature provides lost employer contributions on compensation amounts up to the Section 401(a)(17) income limit. However, employers have the option to extend this true-up contribution to all compensation, allowing executives to receive total employer contributions equal to the same percentage of income that other employees receive through the 401(k) plan.