Nonqualified deferred compensation plans (NQDCPs) are effective, flexible tools to help recruit, reward and retain top talent. Employers determine who participates in these plans, the amount of plan benefits, the timing of when benefits can be received and the vesting schedule applied to any employer contributions.

Participants’ account balances grow tax-deferred, and they can choose to receive benefits without penalty prior to age 59½. However, these plans are technically unfunded from an ERISA standpoint, even if assets are informally set aside to finance plan liabilities. This means that plan benefits are unsecured obligations that are subject to the creditors of the employer in the event of bankruptcy.

Given these significant risks, NQDCPs are not typically offered to all of a company’s employees. The flexibility described above is only available if plan participants are limited to a top hat group, meaning the plan exists “primarily for the purpose of providing deferred compensation for a select group of management or highly compensated employees.”¹ Unlike qualified plans such as 401(k) programs, top hat plans are exempt from ERISA participation, anti-discrimination, vesting, funding and fiduciary requirements.

History

The Department of Labor (DOL) has never provided bright-line guidance for how to define a top hat group. In 1990, DOL Advisory Opinion 90-14A provided some broad guidelines for who may be included in a top hat group. The DOL said that factors such as having management responsibilities, earning high income, having an ability to influence the design of the NQDCP and having an understanding of non-ERISA protected risks such as bankruptcy could all help determine the top hat participant group. However, despite plan sponsors’ desire for greater clarity, the DOL has not provided additional regulations or substantive guidance on this topic since the 1990s.

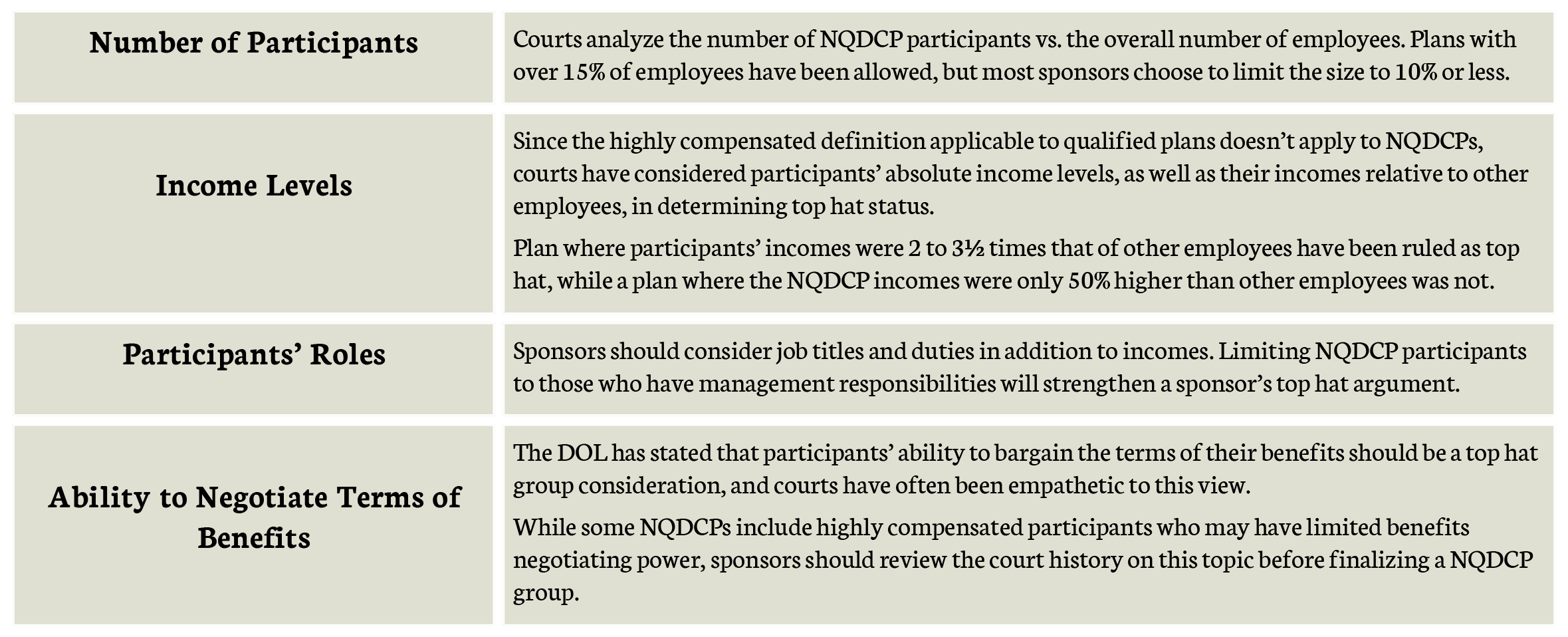

This lack of regulatory guidance has led plan sponsors and their advisors to largely rely on court rulings to develop guidelines for what is likely to qualify as a top hat group. While courts have occasionally come to different conclusions on top hat issues, rulings have generally been consistent enough to develop industry best practices over the years based on case law. Shown below are some of the important topics plan sponsors should consider when determining a top hat group.

Conclusion

Given the fact that the DOL has not issued subsequent regulations or substantive guidance on top hat issues since the 1990s, it seems unlikely it will do so in the near future. In the absence of a bright-line set of rules, plan sponsors must rely on case law and general industry best practices to determine who can participate in a NQDCP.

The more conservative a sponsor is in limiting the group based on income, roles, decision-making capabilities and bargaining power, the more likely it is to be successful if the top hat status of a NQDCP is ever challenged. We recommend that you work closely with your legal counsel to determine who can be part of a top hat group based on the demographics and responsibilities of your specific organization’s key employees.

Wrightwood can help you analyze important top hat considerations throughout this review process.